An ultra cheap quality small cap to consider

Shani Jayamanne | Morningstar

SkyCity (ASX: SKC) is a gambling and entertainment company, owning five casino properties in New Zealand and Australia. The properties include hospitality venues, luxury hotels, a conference and a convention centre.

Star rating: ★★★★★

Moat rating: Narrow

Uncertainty rating: High

Fair Value Estimate: $3.10

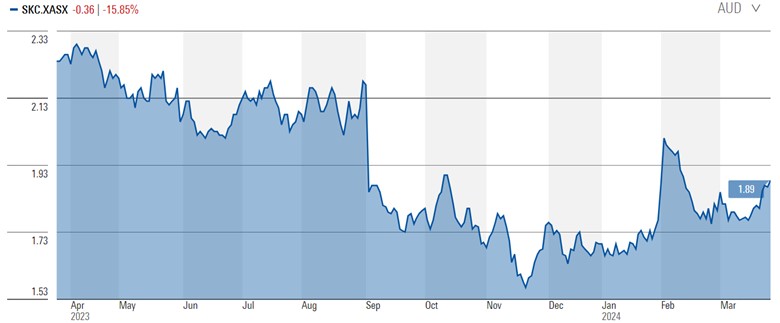

It is currently a five-star stock and extremely undervalued, trading at a 40% discount to its $3.10 fair value estimate. It has been awarded a narrow moat, indicative of our analysts’ confidence in their ability to maintain a sustainable competitive advantage for at least the next ten years.

Source: Morningstar

Our analyst Angus Hewitt expects SkyCity to deliver strong earnings growth over the next decade, buoyed by the recovery from cyclical lows and solid performance from its core assets in Auckland and Adelaide. SkyCity's Auckland and Adelaide properties underpin the firm's narrow economic moat.

SkyCity is the monopoly operator in both jurisdictions, with long-dated licences (exclusive licence for Auckland expires in 2048, and Adelaide licence expires in 2085 with exclusivity guaranteed until 2035). These properties have performed strongly, thanks to SkyCity's solid record of reinvestment, resulting in high property quality, stable visitor growth, and earnings resilience.

To protect its competitive position and retain appeal, SkyCity is investing in its key properties. Successful execution of the two major projects in Auckland and Adelaide is key. They provide good earnings opportunities, in particular at the core Auckland property. This includes a NZD $750 million upgrade to SkyCity Auckland to be completed by calendar 2025 and an AUD $330 million expansion for SkyCity Adelaide, a transformational project completed in fiscal 2021. Beyond 2025, when the Auckland project comes online in full, we expect SkyCity Entertainment to resume generating excess returns and revert to a strongly cash-generating business on a substantially stepped-up earnings base.

We believe SkyCity Entertainment enjoys a narrow economic moat by virtue of its long-dated and exclusive licences in Auckland, New Zealand, and Adelaide, Australia. Stringent regulatory licensing creates barriers to entry for competition, allowing the firm to enjoy economic returns in a regulated environment. We expect returns on invested capital to average 10% during the next decade, comparable with pre-covid-19 returns, exceeding the company's 8% weighted average cost of capital.

Legal barriers to entry protect SkyCity's key assets in Auckland and Adelaide. The company's facilities enjoy a privileged position, boasting long-term monopoly licences from the relevant governments. The Australian and New Zealand casino markets are mature and highly regulated. Australia and New Zealand differ from many other markets in the U.S. and Asia as they do not have large gaming strips or enclaves of casinos, with licences often permitting just one or two casinos per city. This strict licensing regime creates a legal entry barrier, an intangible asset that drives our narrow economic moat rating.

We assign SkyCity a Morningstar Uncertainty Rating of High as a result of the firm's exposure to external factors that can crimp the earnings of its casinos—principally the rate of recovery of gaming in the aftermath of the covid-19 pandemic—and regulatory risks. Regulatory risks are ever present in the gaming sector, including potential tax increases, tighter regulatory oversight, and environmental, social, and governance risks such as gambler harm-minimisation measures.

We assign SkyCity a Standard Morningstar Capital Allocation Rating based on our assessment of balance sheet risk, investment efficacy, and shareholder distribution.

SkyCity's balance sheet is in sound condition. It remains robust, bolstered by a NZD$230 million capital raise completed at the end of fiscal 2020 and extensions to new and existing debt facilities.

Access this research and more at Morningstar. For a free four-week trial, click here.

Shani Jayamanne is an investment specialist, Individual Investor, Morningstar Australia.

All prices and analysis at 25 March 2024. This information has been prepared by Morningstar Australasia Pty Limited (“Morningstar”) ABN: 95 090 665 544 AFSL: 240 892 .

The content is distributed by WealthHub Securities Limited (WSL) (ABN 83 089 718 249)(AFSL No. 230704). WSL is a Market Participant under the ASIC Market Integrity Rules and a wholly owned subsidiary of National Australia Bank Limited (ABN 12 004 044 937)(AFSL No. 230686) (NAB). NAB doesn’t guarantee its subsidiaries’ obligations or performance, or the products or services its subsidiaries offer. This material is intended to provide general advice only. It has been prepared without having regard to or taking into account any particular investor’s objectives, financial situation and/or needs. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation and/or needs, before acting on the advice. Past performance is not a reliable indicator of future performance. Any comments, suggestions or views presented do not reflect the views of WSL and/or NAB. Subject to any terms implied by law and which cannot be excluded, neither WSL nor NAB shall be liable for any errors, omissions, defects or misrepresentations in the information or general advice including any third party sourced data (including by reasons of negligence, negligent misstatement or otherwise) or for any loss or damage (whether direct or indirect) suffered by persons who use or rely on the general advice or information. If any law prohibits the exclusion of such liability, WSL and NAB limit its liability to the re-supply of the information, provided that such limitation is permitted by law and is fair and reasonable. For more information, please click here.