High time to hedge?

Investing across different geographies and currency areas can be a good way to help diversify a portfolio

Historically, the Australian dollar (AUD) has been seen as a ‘risk currency’ relative to the USD, meaning it typically depreciates in response to a negative change in risk sentiment (and vice versa). This means that, for Australian investors in US equities, unhedged exposure has tended to cushion AUD returns in times of market volatility. However, given the extent of recent falls in the market, and as the AUD/USD approaches levels last seen during the onset of the pandemic and back in the Global Financial Crisis, investors are increasingly asking themselves the question – is it ‘high time to hedge’?

International investing often comes with exposure to foreign currency movements, which can have a significant impact on returns. The more volatile the exchange rate between two currencies, the higher the risk and potential impact on returns. For investors wishing to reduce this volatility, currency hedging can help minimise unintended currency bets.

Currency risk arises from the change in price of one currency versus another. In the same way that companies’ shares rise and fall in value, so do currencies, when compared with one another. When buying or selling an investment denominated in a currency different than your base currency, the exchange rate of this foreign currency with the base currency forms part of the investment returns.

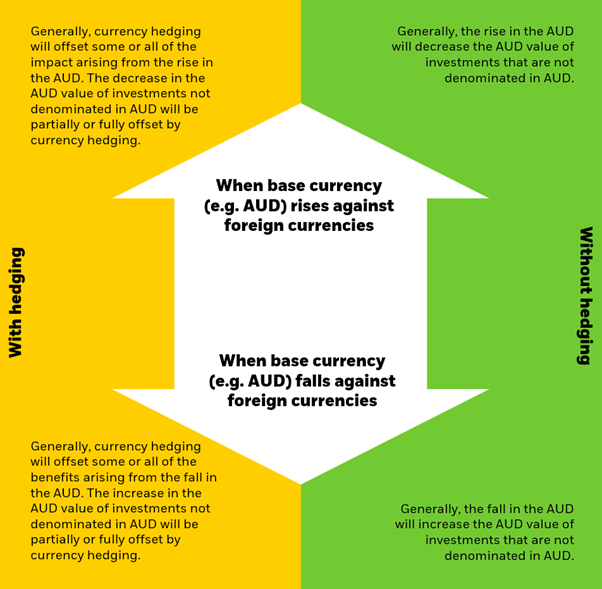

Hedging in currency risk

In the case where an investor might have a negative view on the foreign currency, they may want to get exposure to the underlying market. By hedging the currency risk in their investment, the portfolio is getting exposure to a foreign asset, but without getting exposure to the foreign currency of that asset. Although often overlooked, currency exposures can be significant drivers of risk and returns of a portfolio.

In unhedged exposures, the impact of currency movements can be either positive or negative. The aim of currency hedging is not to capture the positive movements and reduce the negative movements. Instead, it focuses on mitigating the impact of any currency movements on the underlying investment return so that investors’ returns are based on the performance of the underlying asset they sought exposure to.

Effectiveness of hedging under different currencies scenarios

For illustrative purposes only.

Source: iShares

Case study: Equity

An investor managing a AUD based portfolio may wish to gain exposure to the S&P 500 Index. If they do not have a favourable view on USD or simply want to shield the portfolio from USD/AUD volatility, they can choose to hedge the currency risk in this exposure.

For instance, the chart below compares the return of the S&P 500 versus the AUD hedged S&P 500, all in AUD (the currency of the investor’s portfolio).

Since the onset of monetary tightening in the US, USD has been strengthening vs. AUD. Therefore, an unhedged S&P 500 investment would have outperformed the return of the AUD hedged index. Given the extent of recent USD strength and Australia’s favourable position as a commodity exporter in a new era of constrained supply, investors are beginning to question how long this trend can continue.

Source: Bloomberg. Data from 31/12/2014 - 13/10/2022. Performance rebased to 100.

Past performance is not a reliable indicator of current or future results and should not be the sole factor of consideration when selecting a product or strategy. The figures shown relate to past performance. Index performance returns do not reflect any management fees, transaction costs or expenses. Indices are unmanaged and one cannot invest directly in an index.

Case studies are for illustrative purposes only; they are not meant as a guarantee of any future results or experience and should not be interpreted as advice or a recommendation.

Analysis as at 24 January 2023. This information has been provided by BlackRock Investment Management (Australia) Limited ABN 13 006 165 975, AFSL 230 523 (BIMAL), for WealthHub Securities Ltd ABN 83 089 718 249 AFSL No. 230704 (WealthHub Securities, we), a Market Participant under the ASIC Market Integrity Rules and a wholly owned subsidiary of National Australia Bank Limited ABN 12 004 044 937 AFSL 230686 (NAB). Whilst all reasonable care has been taken by WealthHub Securities in reviewing this material, this content does not represent the view or opinions of WealthHub Securities. Any statements as to past performance do not represent future performance. Any advice contained in the Information has been prepared by WealthHub Securities without taking into account your objectives, financial situation or needs. Before acting on any such advice, we recommend that you consider whether it is appropriate for your circumstances.